Blockchain and e-Commerce: A Change For the Better?

It’s no secret that the world of technology at large has been focusing on select buzzwords over the last couple of years or so. The attention is primarily on the macro-level impact of digital technology across multiple industries for the future–blockchain is no different. It is rare, however, when one can explain how these new concepts can impact existing business models TODAY without the need for wider societal adoption. As a result, companies with a focus on e-commerce are most associated with the benefits of blockchain, and its players can benefit from this new ledger-based concept.

So enough of the fluff; what is blockchain?

Without being too technical, blockchain utilizes distributed ledger technology (DLT) to provide transparency in logistics and can be used to archive transactional information. The original intent for creating DLT was to use the technology to archive cryptocurrency transactions in a reliable way. Against the backdrop of a rapidly growing cryptospace where projects were (and apparently still are) popping up on a frequent basis, many didn’t predict that one of the few technologies to withstand this noisy period would be the blockchain itself.

What is the current state of e-commerce?

To understand the benefits that applying blockchain technology can bring for a business in this space, it is important to understand the current state of e-commerce. According to Forbes, e-commerce will account for about 20.4% of total global retail sales by the end of 2022, nearly double what it was five years ago (10%). This shows that e-commerce is becoming increasingly crowded. When looking at the numbers, it’s also easy to see that the pandemic-era lockdowns have significantly boosted the adoption of e-commerce, acting as a catalyst for an already growing space, albeit at a slower pace. It’s basically like boosting the speed of a car that was already in the fast lane.

In April 2021, Amazon posted USD 108.5 Bn in revenue for the first three months of the year, up 44% from a year earlier. The company also posted a profit of USD 8.1 Bn, up 220% year-on-year. Even without knowing these numbers, the impact was evident–it was rare not to see an Amazon Prime van or unopened brown and blue packages on doorsteps bearing the Amazon logo when driving through any residential neighborhood during the lockdown.

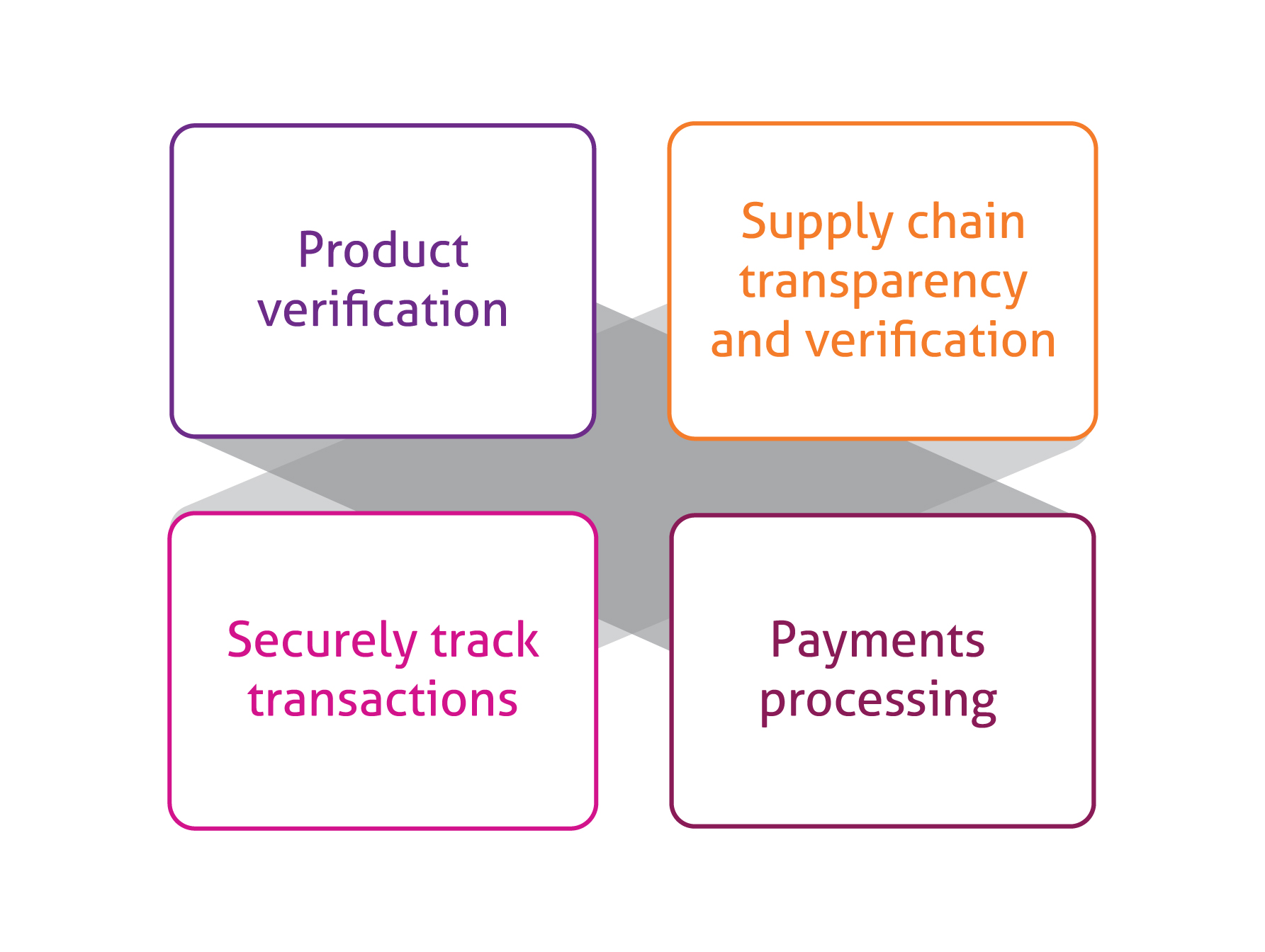

So, what are the difficulties in e-commerce, and how can blockchain help?

An important factor is the aim to create a seamless and trust-free experience. The current norm for any online store is to tell prospective customers that they are trustworthy, and this is done in several ways; testimonials, return policies, or maybe even word of mouth. If you’re lucky, they may even have “trust badges” to ensure their authenticity. They may even have multiple reviews on Trustpilot singing their praises. While we would like to think the best of online retailers, it must be said that these are flimsy criteria used to decide whom you purchase from. Unfortunately, all these can be manipulated in favor of the seller. According to ZDNet, as the number of reviews submitted to Trustpilot increased, so did the number of fake reviews–a 19% increase in the performance of automated detection attempts year over year.

Blockchain aims to remove that feeling of taking a leap of faith with an online store–the idea being when you make a purchase, you know where the product currently is, how much it cost the supplier, its logistical journey as well as a transactional record of the purchase that is on an open protocol that can be accessed by anyone.

Ways blockchain can be applied to e-commerce

There are many household names who have already applied blockchain to their supply chain and operational model. Aside from the likes of UPS, FedEx, and Amazon already reaping the benefits of blockchain in their logistics and supply chains, J.P. Morgan CEO Jamie Dimon has advocated distributed ledger technology as a commercial enterprise operations platform, and incoming Goldman Sachs CEO David Solomon is extolling its virtues as a cryptocurrency-buying and selling mechanism. Walmart, IBM, and almost every principal publicly traded business enterprise is also vying for possibilities to implement the ledger generation in their commercial enterprise plans. Builtin.com lists the following companies as ones who are using distributed ledger technology in their current models:

- IBM (IBM)

- Microsoft (MSFT)

- Oracle (ORCL)

- Intel (INTC)

- Anheuser-Busch InBev (BUD)

- Daimler (DAI)

- Walmart (WMT)

- Goldman Sachs (GS)

- Alibaba (BABA)

In a world where more and more routine tasks are taking on a digital aspect, it’s easy to feel as if things may be moving too quickly to get a thorough read on what’s going on. To echo the opening paragraph, there are simply so many buzzwords being thrown around; you don’t know which one to focus on and when. Therefore, it’s important to zero in on concepts that can bring tangible benefits to a business in the here and now as well as the future–it can be argued that blockchain is one of those concepts. In the old days, when you walked into a store for the first time, you didn’t have to trust that you would receive the item or that your payment was going into the cash register–oh, how times have changed.

Blogger's Profile

Mohamed Ali

Consultant (CX), LTIMindtree

Product owner with close to a decade of experience in various industries such as fintech, publishing, and e-commerce. He has a passion for implementing cutting-edge technologies in his work and is always on the lookout for new ways to improve products and services. Mohamed has a strong background in product management, market research, and product development, which enables him to deliver high-quality products that meet customer needs. He is a natural problem solver and enjoys working closely with clients to identify their pain points and develop solutions that address their needs.

More from Mohamed Ali

These are exciting times–that's certainly one way of stating it. Almost every major company…

Latest Blogs

he supply chain is a network of suppliers, factories, logistics, warehouses, distributers and…

Introduction What if training powerful AI models didn’t have to be slow, expensive, or data-hungry?…

Pharmaceutical marketing has evolved significantly with digital platforms, but strict regulations…

Leveraging the right cloud technology with appropriate strategies can lead to significant cost…